R is for Recovery…or Recession?

With already almost a month and a half behind us in 2023 and the market having bounced nicely to start the year, it is a good time to reassess where we are at, and more importantly, what we think the rest of the year could look like.

Interest Rates/US Economy/Unemployment

This will continue to be front and center as the fight against inflation continues, though we believe we are closer to the end of that battle. We expect inflation to continue to gradually come down and the Fed to have 1-2 more rate increases left in this cycle.

US Consumer. As we wrote last month, consumer spending makes up roughly 70% of the US GDP, so we continue to watch for stresses across the various income demographics as well as the various purchasing categories…

…and while employment numbers in January surprised to the upside, more companies continue to announce layoffs…Disney 7,000 (3% of staff), Dell 6,650 (5% of staff), Zoom 1300 (but 15% of its staff), and Amgen and Johnson & Johnson (though smaller numbers).

Wax on, Wax off. Risk on, Risk off

For over a decade the market has seen a significant shift from active investing to Exchange Traded Funds (ETFs) or similar investment vehicles.

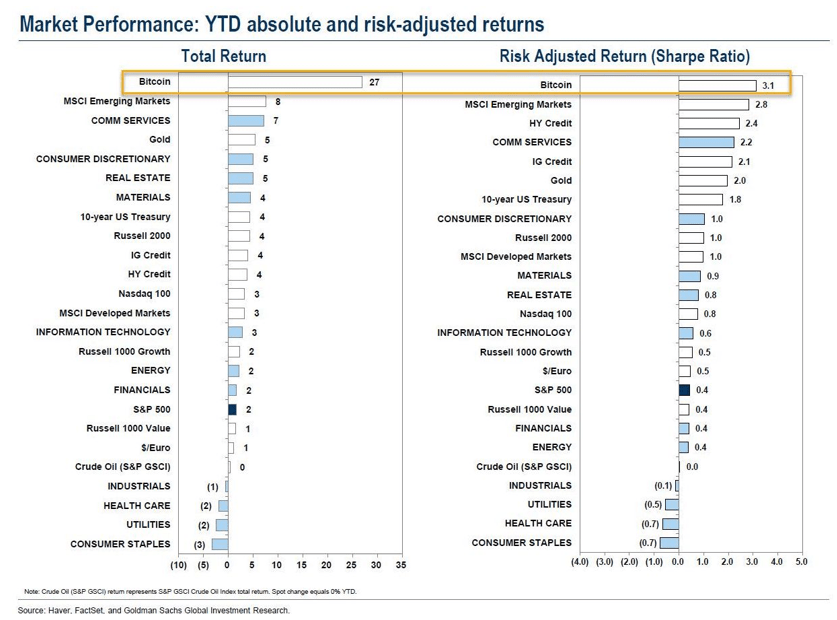

This period has been very challenging for traditional active investment managers in terms of their ability to outperform their benchmarks. A by-product of this has been an “all or nothing” view on the market as well. Many in the industry have used the terms “risk on” and “risk off.” Though there are many market pundits who have been suggesting that this is the year for active management, the returns thus far have shown otherwise. We stumbled upon this chart and wanted to share it with you, as it continues to show the generally binary nature of the market. Basically, the riskiest assets have shown the greatest return, which is almost a mirror image of what took place in 2022.

Patience…being paid to wait.

So what do we favor now? We have often spoken of the market being range bound for at least the first half of the year and we continue to think that will be the case. The range we have discussed has been the S&P500 in the low 3000s to somewhere in the 4200 range at the high end. With the S&P 500 up nearly 7% year to date at 4,090.46 (as of 2/10/23) and the added risk that inflation has a short term re-acceleration, we advocate patience, and with interest rates in various fixed income vehicles ranging from 4 to 5%, investors are being paid nicely to wait for the next opportunity.

Our most recent articles:

- Happy Presidents Day!

- The Health Savings Account (HSA)

- Happy Holidays!

- “There is no way to peace, peace is the way.”

- Hello Fall.