Get Connected

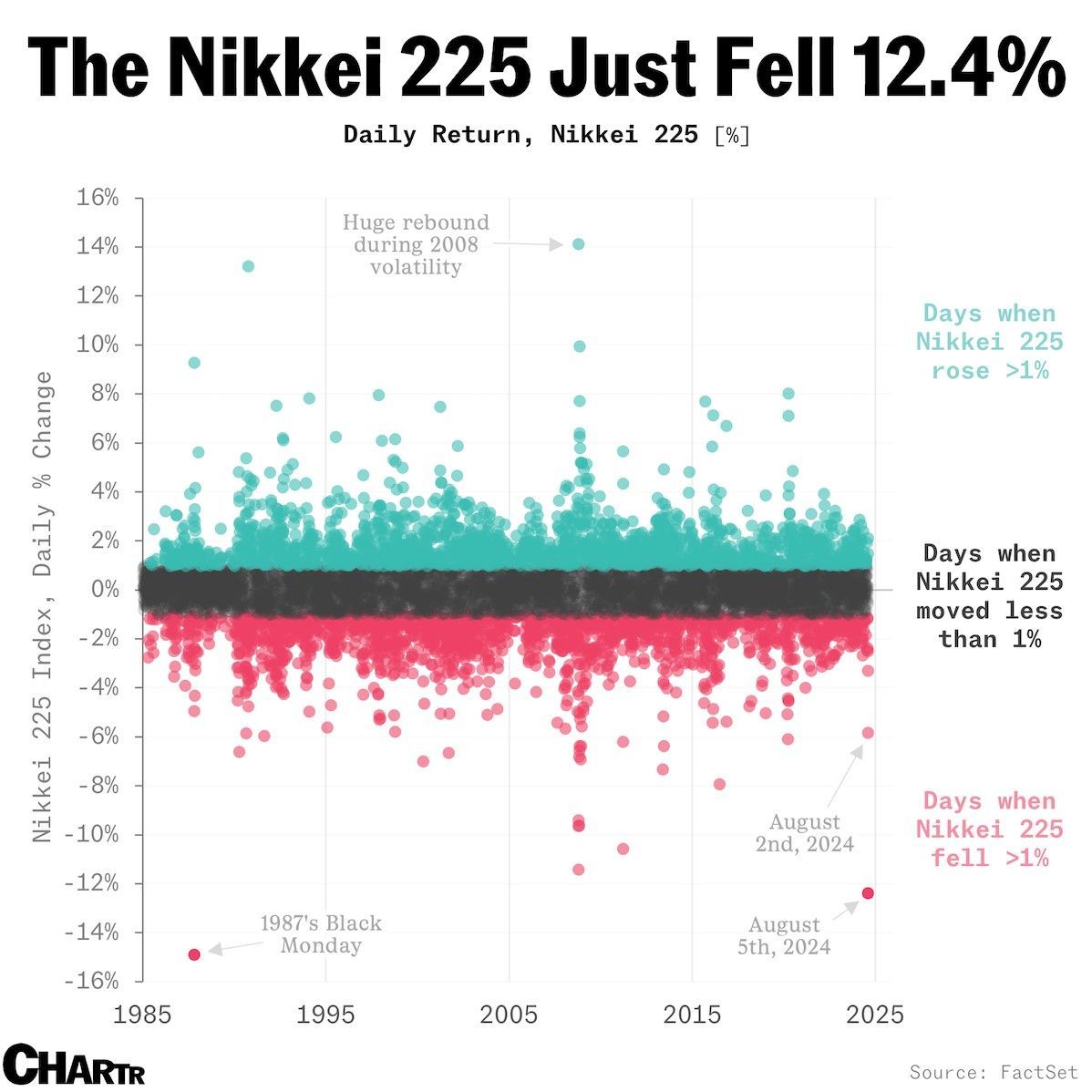

As I sat down on Sunday evening to begin writing the newsletter for August, markets in Asia were indicated down sharply. This morning, we woke up to the Nikkei doing this:

So why is this happening and what does this mean to US stocks?

Japan has for many years now had an extremely low interest rate relative to every country in the world. Because of the low rates, investors would borrow in Japan and re-invest elsewhere to get better returns. This was known as the “carry trade.” Last week the Bank of Japan raised rates and it has caused some issues with regards to this trade as a rapid appreciation in the Japanese Yen against the US Dollar created losses and is forcing an unwind of this trade.

Additionally, while the Japanese economy has exhibited signs of breaking out of its multi-decade economic stagnation, the strong rally in the Japanese market to record highs through the first half of the year reflected hopes that have yet to be substantiated. The US and Japanese economies have not been tightly correlated for many years now, therefore we see little fundamental impact to US companies.

Prior to the recent sell off, the S&P 500 and Nasdaq were up significantly year to date, so it is understandable as to why stocks would sell off as, combined with some recent soft economic data from the US, the markets were set up for some near-term profit taking.

Is the Fed behind the curve? The dreaded “R”-word.

We have always been focused on fundamentals and valuations to determine the potential opportunities in companies or the overall market. While there has been a lot of news around a weaker consumer, a weaker employment report and a weaker ISM report, we are nowhere near “Recession” territory versus some of the expectations 12 months ago. In fact, these weaknesses are exactly what is needed for the Fed to stop raising interest rates and start reducing them. The magnitudes of the negatives are somewhat benign and the main growth driver, Artificial Intelligence/Technology, remains intact as Microsoft, Alphabet and Amazon provided strong cloud outlooks on their calls in the past couple weeks.

In summary, while the economy has shown some signs of finally slowing, this will enable the Fed to start reducing rates and should ultimately provide a floor to the stock market. We will continue to monitor the elections and will have more discussion on that in our monthly newsletter next week. Finally, we do not feel the Fed will cut rates in the interim prior to the next FOMC meeting on 9/18, but there will be plenty of opportunity for Fed officials to make “calming” remarks between now and then with the Jackson Hole Economic Policy Symposium on 8/22-8/24, where Chairman Powell will also have the opportunity to calm markets if necessary.

Quick Links

Contact Details

IMPORTANT DISCLOSURES

Bergamot Asset Management LP (“Bergamot”) is registered with the state of New Jersey as an investment adviser located in Princeton, New Jersey. Bergamot and its representatives are in compliance with the current notice filing requirements imposed upon registered investment advisers by those states in which Bergamot maintains clients. Bergamot may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration requirements. Bergamot’s web site is limited to the dissemination of general information pertaining to its investment advisory services. Accordingly, the publication of Bergamot’s web site on the Internet should not be construed by any consumer and/or prospective client as Bergamot's solicitation to effect, or attempt to effect transactions in securities, or the rendering of personalized investment advice for compensation, over the Internet. Any subsequent, direct communication by Bergamot with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of Bergamot, please contact the state securities law administrators for those states in which Bergamot maintains a notice filing. A copy of Bergamot's current written disclosure statement discussing Bergamot's business operations, services, and fees is available from Bergamot upon written request. Bergamot does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Bergamot's web site or incorporated herein, and takes no responsibility therefor. All such information is provided solely for informational/convenience purposes only and all users thereof should be guided accordingly. Registration of an Investment Adviser does not imply any level of skill or training.

Each client and prospective client agrees, as a condition precedent to his/her/its access to Bergamot’s web site, to release and hold harmless Bergamot, its officers, directors, owners, employees and agents from any and all adverse consequences resulting from any of his/her/its actions and/or omissions which are independent of his/her/its receipt of personalized individual advice from Bergamot.

The information contained herein reflects the opinion and projections of Bergamot as of the date of publication, which are subject to change without notice at any time subsequent to the date of issue. Bergamot does not represent that any opinion or projection will be realized. All information provided is for informational purposes only and should not be deemed as legal, tax, investment advice or a recommendation to purchase or sell any specific security. This shall not constitute an offer to sell or the solicitation of an offer to buy any interest in any fund managed by Bergamot or any of its affiliates. While the information presented herein is believed to be reliable, no representation or warranty is made concerning the accuracy of any data presented. Market conditions can vary widely over time and can result in a loss of portfolio value. Past performance does not guarantee future results.